Credit & Loans

Video link: https://youtu.be/W9UJB-7om8c

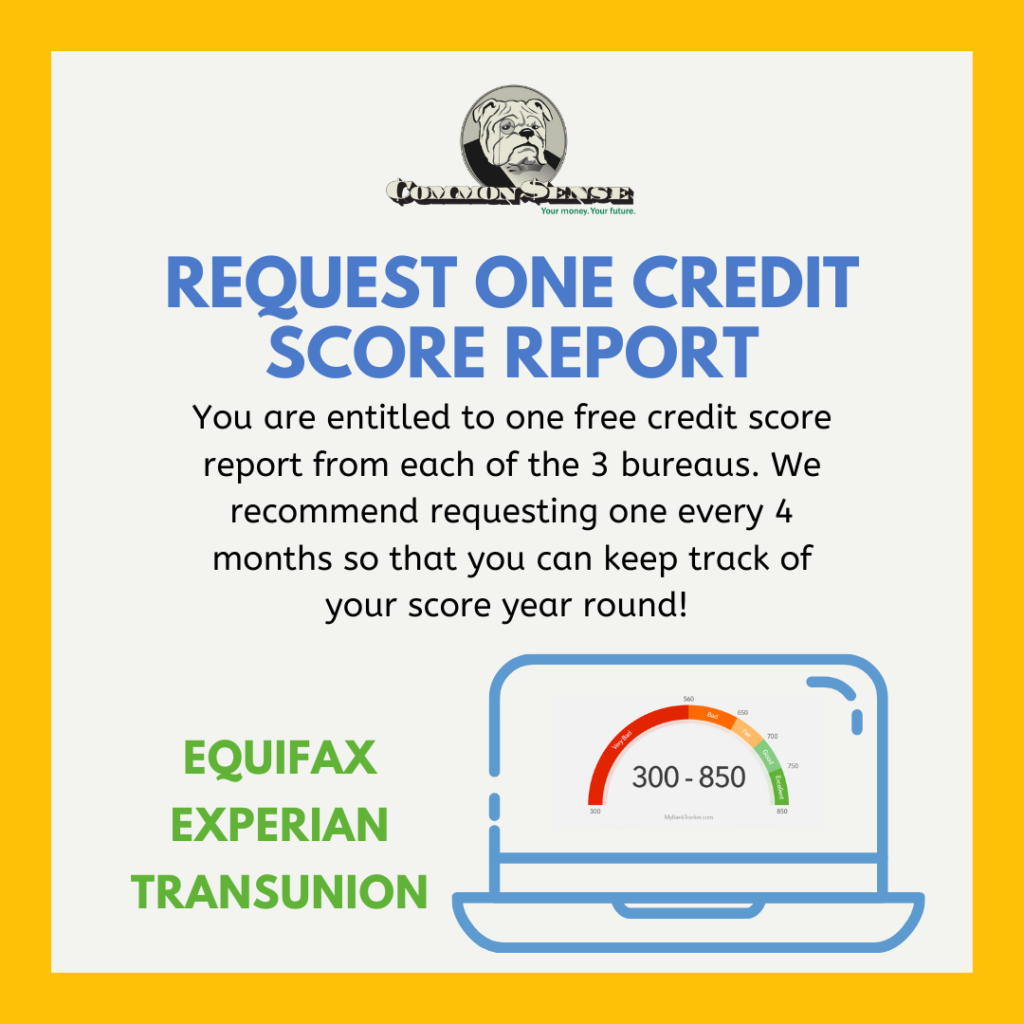

What is credit and how do you build it?

Credit is the ability to borrow money or access goods or services with the understanding that you’ll pay later (Experian). People that have a social security number and/or a Tax ID number qualify for taking out loans/credit cards, therefore they are able to build a credit score. Credit scores are calculated based on payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%) (myFico). The easiest way to build your credit is through credit cards and another common way is through loans. The best way to ensure that you have a positive credit record is to always make payments in a timely manner, pay more than the minimum payment (all if possible), and only spend a portion (11%) of credit available to you. Keep in mind that your credit score determines your eligibility and rates for things such as private loans, mortgages, car payments, even some jobs. Therefore, it is always important to monitor your score shown below and maybe use a company such as Credit Karma to keep track of your estimated credit score.

Important Note: when a potential lender (i.e. bank) has to pull your credit report in order to see if you qualify for a credit card/loan it can temporarily decrease your score so beware of applying for too many loans at the same time!

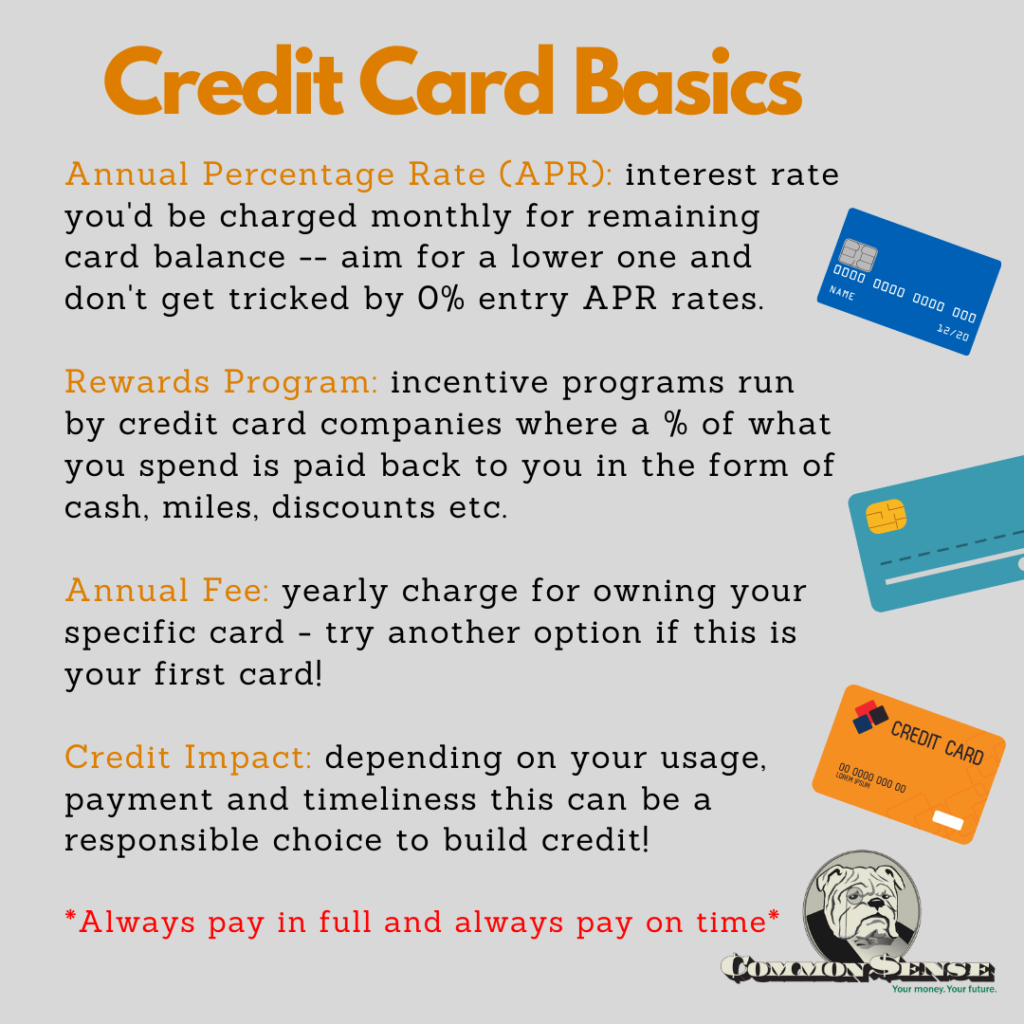

How do credit cards work and should you get one?

Credit cards aren’t for everyone. However, they can be a powerful tool for building your credit. Below are some basics when examining different types of credit cards. Just make sure that if you do utilize one, do not spend beyond your means and always pay off the balance in full if possible!

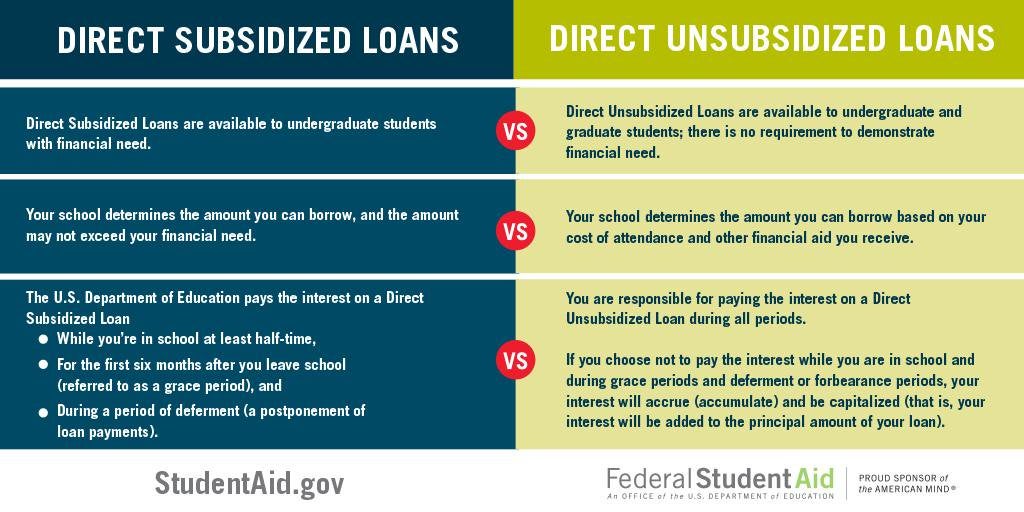

How do Federal Direct Student Loans work?

If you are eligible, you will be offered federal direct loans and the chart above can show you key differences between both loans. Regardless of the loan type, once you graduate, drop below half-time enrollment or leave, you will have a 6 month “grace period” (a time when you don’t have to start repaying). Once repayment begins it will be up to your lender to provide a schedule for your payments. Don’t fret to much if you go back to school or can’t meet your monthly payments, there are guidelines on studentaid.gov that will help you through the repayment process.